TL;DR:

- Moldova offers simple, remote company registration that automatically grants corporate residency at no wait.

- Standard companies face a 12% tax on worldwide profits, while IT firms can benefit from a 7% unified tax under MITP.

- Long-term success depends on maintaining genuine local operations and compliant substance, not just initial setup.

Most international entrepreneurs assume that establishing corporate residency in Moldova involves bureaucratic complexity, lengthy waiting periods, or a permanent on-the-ground presence. The reality is quite different. Moldova has built one of Eastern Europe’s most accessible corporate frameworks, with a standard 12% corporate income tax and a remarkable 7% unified tax rate for IT companies operating through the Moldova Innovation Technology Park. This guide breaks down exactly how corporate residency works, which tax regime suits your business, how to handle edge cases like dual residency, and what ongoing compliance actually looks like in practice.

Table of Contents

- What corporate residency means in Moldova

- Standard tax regime for Moldovan resident companies

- Special tax regime for IT companies: The MITP advantage

- Edge cases: Permanent establishment, dual residency and substance requirements

- How to obtain and maintain Moldovan corporate residency

- What most guides miss: The real success factors for Moldova corporate residency

- Ready to build your company in Moldova?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Residency via incorporation | Registering your company in Moldova makes it a tax resident, regardless of management location. |

| Standard rate is 12% | Resident companies pay 12% on net worldwide profits unless qualifying for special regimes. |

| MITP offers unique benefits | IT firms can access a 7% unified tax regime that simplifies and reduces total liability. |

| Substance is essential | Having real activities and employees is key to securing and keeping residency benefits. |

| Practical steps required | A clear process—incorporate, apply for regimes, and maintain compliance—ensures ongoing corporate residency. |

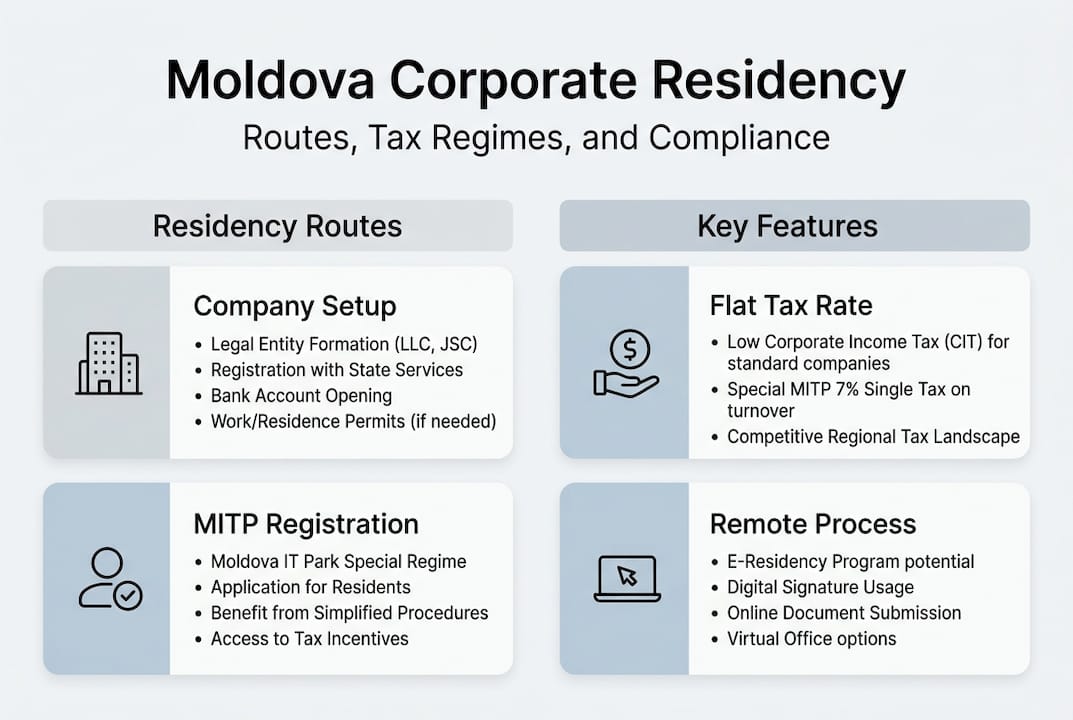

What corporate residency means in Moldova

Corporate residency is the legal status that determines where a company is taxed on its profits. In Moldova, this concept is straightforward: a company is tax resident if it is organised or managed in Moldova, or has its main place of business there, with residency primarily determined by place of incorporation.

This means the moment you complete the incorporation process and register your SRL (Societate cu Răspundere Limitată, Moldova’s standard limited liability company structure) with the State Registration Chamber, your company automatically becomes a Moldovan tax resident. No waiting period. No secondary approval.

Here is what that residency status practically involves:

- Automatic tax residency upon registering your SRL with local authorities

- Worldwide income taxation applies from the date of incorporation

- No immediate physical presence required at the outset, though substance becomes important later

- Management and control criteria can also establish residency for foreign-incorporated entities

- Certificate of residency is issued upon registration and used for treaty purposes

Where confusion commonly arises is the distinction between establishing residency and maintaining beneficial tax status. Registering is simple. But accessing specific tax regimes, such as the MITP (more on that shortly), requires additional steps and ongoing substance.

Pro Tip: Before registering, review the formation checklist to ensure you have all required documents prepared. Missing a single item can delay your registration by weeks.

| Step | Action | Outcome |

|---|---|---|

| 1 | Register SRL with ASP | Automatic corporate residency |

| 2 | Obtain tax identification number | Enables filing and banking |

| 3 | Open a corporate bank account | Operational readiness |

| 4 | Apply for MITP (if IT company) | Preferred tax regime access |

Most international founders are surprised to learn that the entire registration process can be completed remotely via Power of Attorney, without ever boarding a flight to Chișinău.

Standard tax regime for Moldovan resident companies

Once your company holds Moldovan corporate residency, it is subject to Moldovan tax law on all income, regardless of where that income is earned. Tax resident companies are taxed on worldwide income at 12% corporate income tax (CIT) on net profit.

For context, Romania sits at 16% CIT, Ukraine at 18%, and Germany above 30% including trade tax. Moldova’s 12% positions it competitively across the region without requiring complex holding structures to achieve a reasonable effective rate.

Here is what compliance under the standard regime involves:

- Annual CIT return filed by 25 March of the following year

- Quarterly advance payments based on prior year tax liability

- Bookkeeping under Moldovan National Accounting Standards or IFRS for larger entities

- VAT registration mandatory when annual turnover exceeds 1.2 million Moldovan lei

- Dividend withholding tax applies at 6% when profits are distributed

One detail many founders overlook: net profit means profit after deducting allowable business expenses. Moldova permits standard deductions for salaries, rent, depreciation, and other operational costs, which meaningfully reduces the taxable base.

Key figure: Moldova’s 12% CIT is among the lowest standard rates in Eastern Europe, and profits that are reinvested rather than distributed are taxed at 0%, offering a significant incentive for growth-focused companies.

Pro Tip: Keep detailed records of all business expenses from day one. Moldovan tax authorities conduct routine checks, and well-organised documentation will protect you during any review of your registration steps and tax details.

The standard regime works well for trading companies, holding structures, and businesses whose revenue does not qualify under MITP. For IT-focused operations, however, a far more attractive option exists.

Special tax regime for IT companies: The MITP advantage

The Moldova Innovation Technology Park (MITP) is one of the most genuinely competitive IT tax regimes in Europe. Rather than navigating CIT, VAT, social contributions, and payroll taxes separately, MITP consolidates everything into a single obligation. MITP provides a 7% unified tax on gross turnover, replacing CIT, VAT, social contributions, and other taxes, with 2,725 IT companies now benefiting from the regime.

That single figure of 7% on gross turnover is what makes Moldova so attractive to software developers, SaaS companies, and IT service providers. There is no separate VAT return. No complex payroll tax calculation. One rate, one filing.

To qualify for MITP, your company must meet the following criteria:

- Be registered as a Moldovan SRL

- Generate at least 70% of revenue from qualifying IT activities (software development, IT consulting, data processing, etc.)

- Maintain a minimum number of employees (currently at least one)

- Remain financially solvent with no outstanding tax debts

- Apply separately to MITP after completing standard company registration

The IT tax advantages in Moldova extend beyond the 7% rate. Employees within MITP companies also benefit from reduced income tax obligations, making it easier to attract and retain technical talent locally.

| Feature | Standard CIT regime | MITP regime |

|---|---|---|

| Corporate income tax | 12% on net profit | Included in 7% unified tax |

| VAT | 20% (standard rate) | Replaced by unified tax |

| Social contributions | Separate obligation | Replaced by unified tax |

| Payroll tax | Standard rates apply | Significantly reduced |

| Best suited for | Trading, holding, finance | IT, SaaS, software, tech |

Many founders who discover why IT companies choose Moldova are initially sceptical that a legitimate tax rate this low exists within a European jurisdiction. It does, and it is fully compliant with Moldovan law. The substance requirements are the real commitment, not the paperwork.

Edge cases: Permanent establishment, dual residency and substance requirements

Not every company’s situation is straightforward. Cross-border structures introduce complications that require careful planning.

A foreign company can inadvertently become a Moldovan Permanent Establishment (PE) through certain activities. A PE for non-residents is defined as a fixed place of business or dependent agent in Moldova; Double Tax Treaties (DTTs) help resolve dual residency, and substance is needed for any real tax advantage.

Common scenarios that trigger PE status include:

- Maintaining a physical office or warehouse in Moldova

- Employing staff in Moldova who conclude contracts on behalf of the foreign parent

- A dependent agent habitually exercising authority to bind the foreign company

- Construction or project activity exceeding 9 months

Dual residency, where a company is technically resident in two jurisdictions, is resolved through Moldova’s network of Double Tax Treaties. Moldova has concluded DTTs with over 50 countries, and tie-breaker provisions generally favour the jurisdiction of effective management.

| Issue | Resolution mechanism | Key factor |

|---|---|---|

| Dual residency | DTT tie-breaker clause | Place of effective management |

| PE exposure | Fixed place or agent test | Nature of local activity |

| Treaty benefit access | Substance review | Real employees, real activity |

The incorporation and cross-border issues that catch most multinationals off guard involve substance. Authorities are increasingly scrutinising whether a company’s Moldovan presence is genuine or simply a tax optimisation vehicle with no real activity behind it.

How to obtain and maintain Moldovan corporate residency

Practical clarity is what most founders need at this stage. Here is the step-by-step process for establishing and sustaining Moldovan corporate residency.

- Register your SRL via ASP (Agenția Servicii Publice, Moldova’s Public Services Agency). This single step triggers incorporation via ASP grants residency automatically, with the MITP application as a follow-up step and substance checks performed for regime qualification.

- Obtain your tax identification number and certificate of residency from the State Tax Service.

- Establish a management structure with clearly defined directors and a registered address in Moldova.

- Apply for MITP (if applicable) after completing standard registration. Submit qualifying revenue documentation and confirm staff numbers.

- Hire locally or appoint a local manager to satisfy substance requirements for preferred tax regimes.

- File annual returns by the required deadlines and maintain accounting records throughout the year.

The full setup guide walks through each step in detail, including document requirements for non-resident founders. For those starting from scratch, the ultimate company formation guide provides a thorough overview of the entire process.

Pro Tip: Do not apply for MITP status on day one if your revenue stream is not yet demonstrably IT-sourced. Authorities review qualifying revenue, and an early rejection can complicate a later application. Build your revenue documentation first.

Maintaining residency is not passive. Annual compliance, substance preservation, and timely filings are what keep your preferred tax status intact over the long term.

What most guides miss: The real success factors for Moldova corporate residency

After years of helping international companies set up in Moldova, a clear pattern emerges: founders who focus only on the initial paperwork often encounter difficulties 12 to 18 months later.

The real work is not incorporation. It is building a credible operational presence that survives scrutiny. Moldova’s tax authorities are actively tightening substance checks, particularly for MITP participants. A company with no local employees, no local contracts, and no genuine activity will not retain its 7% rate indefinitely.

The companies that succeed long-term treat company formation advice as the beginning of a compliance journey, not the end of a legal formality. They hire locally, maintain genuine management in Moldova, and document their qualifying revenue carefully.

Speed and low cost are attractive entry points. But sustainability, meaning legal, fiscal, and operational sustainability, is what protects your investment over time. The MITP regime is a genuine advantage, not a loophole, and it rewards companies that commit real resources to the jurisdiction.

Ready to build your company in Moldova?

If this guide has clarified the mechanics of Moldovan corporate residency for you, the next step is moving from understanding to action. Start with your comprehensive formation checklist to confirm you have everything in place before submitting your registration. IT founders should go directly to the dedicated IT setup guide for a tailored walkthrough of the MITP application process. For companies with complex cross-border structures, compliance questions, or sector-specific licensing needs, the team at Incorpore.md is available to provide expert guidance and handle the entire formation process on your behalf, remotely and efficiently.

Frequently asked questions

Do I need to live in Moldova to establish corporate residency for my company?

No, physical presence is not initially required. Incorporation grants residency automatically upon SRL registration, though substance will be needed to access and retain preferred tax regimes.

How is corporate tax calculated for Moldovan resident companies?

Resident companies pay 12% CIT on worldwide net profit under the standard regime, unless they qualify for and apply to the MITP unified tax regime.

What are the main requirements to qualify for the MITP tax regime?

Eligibility requires SRL registration, 70% qualifying IT revenue, a minimum number of employees, and ongoing financial solvency with no outstanding tax debts.

How are edge cases like dual residency and PE resolved?

Moldova applies DTT tie-breakers and substance checks for dual residency, while Permanent Establishments are taxed only on Moldova-sourced income attributable to the PE.